Introduction – I’m 25 and Earning ₹30k a Month — How Should I Start Investing for Long-Term Growth?

If you’re 25 years old, earning ₹30,000 a month, and staring at your bank account wondering “where do I even begin?” — you’re not alone. Most 25-year-olds in India feel the same confusion. Rent, groceries, weekend plans, and suddenly the month is over and savings are ₹0.

But here’s the truth nobody tells you early enough: 25 is the single best age to start investing. Not 30. Not “once you earn more.” Right now.

This article will show you exactly how to start investing on a ₹30,000 salary — step by step, no jargon, no overwhelming theory. By the end, you’ll know where your money should go, how much, and how to actually start today.

Table of Contents

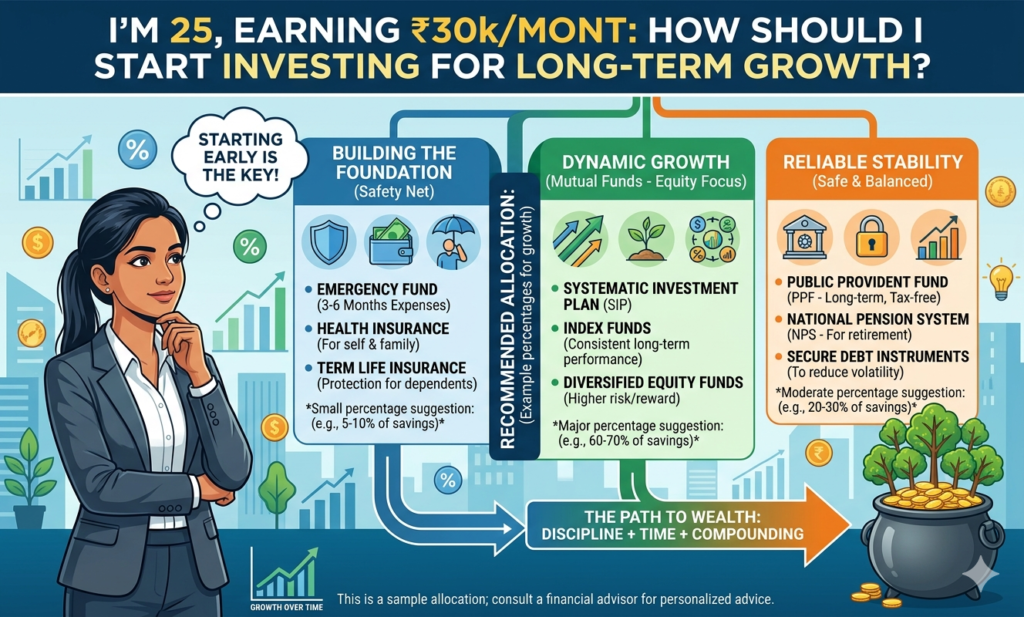

Before You Invest: 3 Things You Must Do First

Jumping straight into stocks or mutual funds without a financial foundation is like building a house on sand. Before investing a single rupee, make sure these three things are in place.

1. Build an Emergency Fund

An emergency fund is 3–6 months of your monthly expenses kept in a liquid savings account or liquid mutual fund — money you can access within 24 hours.

On a ₹30k salary, your monthly expenses are probably around ₹18,000–₹22,000. That means your emergency fund target should be ₹60,000 to ₹1,20,000.

Keep this in a high-interest savings account (like a Small Finance Bank offering 6–7% interest) or a liquid fund. Don’t touch it unless it’s a genuine emergency.

2. Get Health Insurance

If you’re not covered under your employer’s group health insurance — or even if you are — get a personal health insurance policy. A single hospitalisation can wipe out months of savings and investments.

A basic ₹5 lakh cover for a healthy 25-year-old costs roughly ₹5,000–₹8,000 per year. That’s less than ₹700/month for financial protection.

3. Clear High-Interest Debt

If you have any credit card debt or personal loans charging 18–36% annual interest, pay those off before investing. No investment gives you guaranteed 20%+ returns, but your debt is costing you exactly that. Clearing it is the best investment you can make right now.

How to Budget ₹30,000 for Investing

Once your foundation is in place, use the 50-30-20 rule adapted for a ₹30k salary:

| Category | Percentage | Amount |

|---|---|---|

| Needs (rent, food, utilities, transport) | 50% | ₹15,000 |

| Wants (eating out, entertainment, shopping) | 30% | ₹9,000 |

| Savings + Investments | 20% | ₹6,000 |

So realistically, ₹6,000 per month is your investment budget.

If you’re living with family and have lower expenses, you might manage ₹8,000–₹10,000. Even if you can only spare ₹2,000–₹3,000 to start, that is absolutely fine. The habit matters more than the amount in the beginning.

Best Investment Options for a 25-Year-Old in India (2025)

Here’s a breakdown of the best instruments for someone in your position — young, long time horizon, just starting out.

1. SIP in Equity Mutual Funds (Most Recommended)

A Systematic Investment Plan (SIP) lets you invest a fixed amount every month in a mutual fund. Equity mutual funds invest in stocks and historically deliver 12–15% annual returns over the long term.

Why it’s perfect at 25:

- You can start with as little as ₹500/month

- Rupee cost averaging reduces risk — you buy more units when prices are low

- Compounding works best over 20–30 year horizons

- Fully automated — money auto-debits every month

Where to invest: Use platforms like Zerodha Coin, Groww, or Paytm Money. Choose direct plans (not regular plans) to avoid paying distributor commissions.

Recommended categories:

- Large-cap index funds (Nifty 50 or Sensex index fund) — for core, stable growth

- Flexi-cap funds — for slightly higher returns with managed diversification

- Avoid sectoral/thematic funds as a beginner

2. Public Provident Fund (PPF)

PPF is a government-backed savings scheme with a current interest rate of 7.1% per annum (tax-free). It has a 15-year lock-in period, which sounds long but is perfect when you’re 25 — you’ll be 40 and sitting on a solid debt corpus.

Why include PPF:

- Interest is completely tax-free

- Investment up to ₹1.5 lakh per year qualifies for tax deduction under Section 80C

- Zero risk — government guaranteed

- Minimum investment: ₹500/year

You can open a PPF account online through most major banks (SBI, HDFC, ICICI) or India Post.

3. ELSS Mutual Funds (Tax Saving)

Equity Linked Savings Scheme (ELSS) funds are equity mutual funds with a 3-year lock-in period. They qualify for tax deduction under Section 80C (up to ₹1.5 lakh per year).

Since they invest in equities, their potential returns (12–15% historically) are much higher than traditional tax-saving instruments like FDs or NSC.

If you’re in the 20% or 30% tax bracket, ELSS can save you ₹15,000–₹46,000 in taxes annually while also growing your wealth.

4. National Pension System (NPS)

NPS is a government-run retirement scheme where your money is invested in a mix of equities and government bonds.

- Additional tax deduction of ₹50,000 under Section 80CCD(1B) — over and above the ₹1.5 lakh 80C limit

- Partial withdrawal allowed after 3 years for specific reasons

- At 60, you can withdraw 60% of the corpus tax-free; the remaining 40% goes into an annuity

At 25, starting NPS with even ₹1,000/month can build a significant retirement corpus by 60.

5. What to Avoid as a Beginner

- Direct stocks — great long-term, but needs research and emotional discipline. Start after 1–2 years of investing experience.

- Crypto — highly speculative. Not suitable as a core investment.

- Insurance-cum-investment plans (ULIPs, endowment) — poor returns and high charges. Separate insurance and investments.

- Chit funds or “high-return” schemes — if someone promises guaranteed 20%+ returns, walk away.

Sample Investment Plan: ₹6,000/Month at 25

Here’s how you could allocate your ₹6,000 monthly investment budget:

| Instrument | Monthly Amount | Purpose |

|---|---|---|

| Nifty 50 Index Fund SIP | ₹2,500 | Core long-term growth |

| ELSS Fund SIP | ₹2,000 | Equity growth + tax saving |

| PPF | ₹1,000 | Safe debt component + tax saving |

| NPS | ₹500 | Retirement corpus |

| Total | ₹6,000 |

As your salary increases, increase your SIP proportionally. A good rule: increase your SIP by 10% every year.

The Compound Interest Reality Check

Let’s see what ₹6,000/month invested from age 25 actually becomes:

| Duration | Total Invested | Estimated Value (12% returns) |

|---|---|---|

| 10 years (age 35) | ₹7.2 lakh | ₹13.9 lakh |

| 20 years (age 45) | ₹14.4 lakh | ₹59.7 lakh |

| 30 years (age 55) | ₹21.6 lakh | ₹2.1 crore |

| 35 years (age 60) | ₹25.2 lakh | ₹3.8 crore |

You invested ₹25.2 lakh over 35 years and got back ₹3.8 crore. That’s the power of compounding — and it only works this dramatically if you start early.

If you wait until 30 to start (just 5 years later), that same ₹3.8 crore drops to roughly ₹2.1 crore. Starting at 25 gives you ₹1.7 crore extra for the same monthly investment.

Step-by-Step: How to Start Your First SIP Today

- Complete KYC — Visit the KRA (KYC Registration Agency) website or do it through Groww/Zerodha app. You’ll need PAN, Aadhaar, and a selfie.

- Link your bank account — Add your savings account on the investment platform.

- Choose your first fund — For a complete beginner: Nifty 50 Index Fund (Nippon, UTI, or HDFC offer good ones with low expense ratio).

- Set up SIP — Choose the amount (start with ₹500–₹1,000 if nervous), pick a date (usually your salary credit date + 3 days), and confirm.

- Do not touch it — This is the most important step. Don’t check NAV every day. Don’t stop SIP when markets fall. Let compounding do its job.

Total time to set up your first SIP: 15 minutes.

Frequently Asked Questions

- Can I start investing with just ₹500/month on a ₹30k salary?

Yes, absolutely. Many mutual funds and SIPs allow investments starting from ₹100–₹500 per month. The amount matters less than the habit. Start with ₹500, prove to yourself you can do it consistently, then increase the amount every 6 months.

- Should I invest in stocks directly or mutual funds?

For a complete beginner, start with mutual funds — specifically index funds and diversified equity funds. Direct stock investing requires time, research, and emotional discipline. After 1–2 years of investing in funds, you’ll have better understanding to try individual stocks if you want.

- Is it safe to invest in mutual funds? What if I lose money?

Equity mutual funds are market-linked and can go down in the short term. However, over any 10+ year period, a diversified equity fund has historically never given negative returns in India. The risk reduces significantly with time. For a 25-year-old with a 25–35 year horizon, short-term drops are actually opportunities to buy more units at lower prices.

- How much should a 25-year-old invest per month?

A common guideline is to invest at least 20% of your take-home salary. On ₹30,000, that’s ₹6,000/month. If you can manage more — great. If you can only do ₹2,000 right now, that’s still far better than ₹0.

- PPF vs ELSS — which is better for tax saving?

If you’re in the 20%+ tax bracket and have a long investment horizon (10+ years), ELSS is better because of its higher return potential. PPF is better if you want guaranteed, risk-free returns and are in the lower tax bracket. Ideally, use both — ELSS for growth, PPF for stability.

Final Thoughts

The best time to start investing was yesterday. The second best time is today.

At 25, earning ₹30,000 a month, you have the one asset that no amount of money can buy later: time. Every month you delay is compounding working for someone else instead of you.

You don’t need to understand every financial product. You don’t need a large salary. You just need to start — with ₹500, with an index fund, with a SIP set on auto-debit — and then get out of the way and let compounding work.

Your 55-year-old self will thank you.